The Addis Ababa Action Agenda commitments brings the financial inclusion and regulatory agendas together, by acknowledging the implication of regulations on access to financial services, while also noting the importance of robust risk-based regulatory frameworks for all financial intermediation. Inclusive finance strives to enhance access to and usage of financial services for both individuals and Micro, small and medium-sized enterprises (MSMEs).

The Addis Agenda specifically:

- Commits to work towards full and equal access to formal financial services for all

- Commits to adopt or review financial inclusion strategies, in consultation with relevant stakeholders, and to consider including financial inclusion as a policy objective in financial regulation, in accordance with national priorities and legislation

- Encourages commercial banking systems to serve all, including women

- Supports microfinance institutions, development banks, agricultural banks, mobile network operators, agent networks, cooperatives, postal banks and savings banks as appropriate

- Commits to promoting affordable and stable access to credit to MSMEs

- Encourages international and national development banks to promote finance for SMEs, noting the IFC, including through the creation of credit lines

- Recognizes that financial regulations can permit collateral substitutes, create appropriate exceptions to capital requirements, reduce entry and exit costs to increase competition and allow microfinance to mobilize savings by receiving deposits

- Commits to strengthen capacity for cost-effective credit evaluation, including through public training programmes, and through establishing credit bureaux where appropriate

- Commits to providing adequate skills development training for all, particularly for youth and entrepreneurs

- Encourages the use of innovative tools, including mobile networks, banking, payment platforms and digitalized payments

- Recognizes the potential of new investment vehicles, such as development-oriented venture capital funds, blended finance, risk mitigation instruments and innovative funding structures

- Promotes financial literacy

- Expands peer learning and experience-sharing among countries and regions, including through the Alliance for Financial Inclusion and regional organizations

- Commits to strengthening capacity development, including through the UN development system, and encourage collaboration between initiatives

- Acknowledges the importance of regulation to cover all financial intermediation (e.g., shadow banking as well as microfinance)

- Commits to work to ensure that policy and regulatory environment supports financial market stability and promotes financial inclusion in a balanced manner

Latest developments

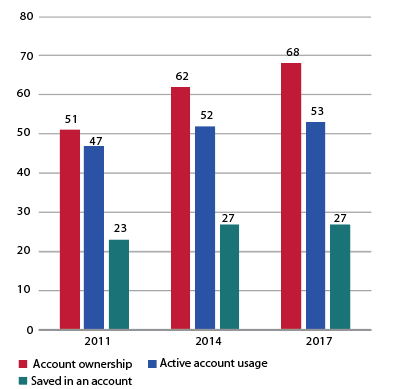

Without adequate financial services, individuals and companies are unable to fully participate in the economy. In recent years, fintech developments— and particularly mobile money services—have contributed to a rapid increase in account ownership and facilitated financing for micro- small and medium-sized enterprises (MSMEs). Nonetheless, about 1.7 billion adults remain unbanked, and important access gaps persist between men and women, poorer and richer households and rural and urban populations. For example, the financial inclusion gender gap in developing countries remained at 9 percentage points in 2017, unchanged since 2011. Active account usage, as measured by a minimum of one deposit or withdrawal per year, also increased at a slower rate than account ownership.

Account ownership and usage, 2011–2017

(Percentage of adults age 15 and above)

Source: World Bank, Global Findex Database.

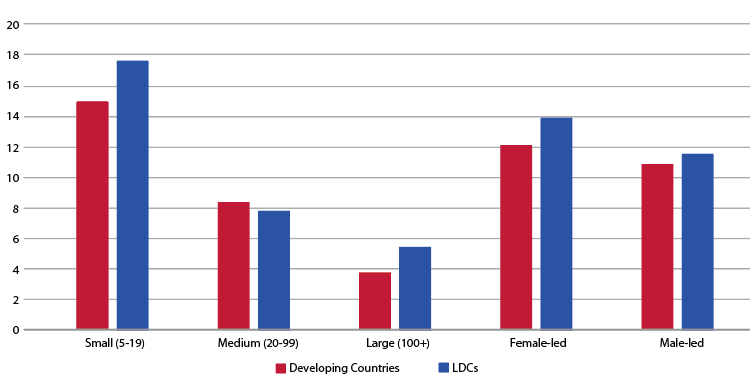

About 131 million or 41 per cent of formal MSMEs in developing countries have unmet financing needs. Globally, MSMEs receive less credit, and their loan applications are more frequently rejected than those of large firms. A much greater share of MSMEs identifies access to finance as a major constraint in comparison to large firms, and women-owned/led firms are more often affected by financing constraints. These discrepancies are more pronounced in LDCs, where financial sectors tend to be less developed.

Percentage of rms whose recent loan application was rejected, ca. 2013

Source: UN DESA, based on World Bank, Enterprise Surveys.

Governments can identify gaps and implement a coherent set of policies to promote solutions that improve financial services to underserved individuals and companies through national financial inclusion strategies, as part of integrated national financing frameworks. Such financial inclusion strategies have been adopted or are being developed by at least 69 countries. Some countries have begun to review past progress and implementation gaps to adjust their strategies to new developments, including fintech. The international community should help countries in developing these strategies.

Read more on addressing financial constraints here.

Relevant SDG indicator

- 1.4.1 Proportion of population living in households with access to basic services

- 8.10.1 Number of commercial bank branches and automated teller machines (ATMs) per 100,000 adults

- 8.10.2 Proportion of adults (15 years and older) with an account at a bank or other financial institution or with a mobile-money-service provider

- 9.3.2 Proportion of small-scale industries with a loan or line of credit