The Addis Ababa Action Agenda commits to incentivizing the expansion of direct investment/foreign direct investment (FDI) to underfunded countries and priority sectors, while ensuring the maximum contribution to sustainable development and other national and regional goals.

Specifically, the Addis Agenda:

- Strengthens efforts to incentivize FDI and address financing gaps and low levels of FDI in developing countries, particularly least developed countries, landlocked developing countries, small island developing States and countries in conflict and post conflict situations

- Acknowledges that foreign direct investment is concentrated in a few sectors in many developing countries and often bypasses countries most in need, and international capital flows are often short-term oriented

- Commits to adopt and implement investment promotion regimes for LDCs

- Encourages the alignment of FDI with national and regional sustainable development strategies; promotes policies to strengthen spillovers as well as integration into value chains

- Encourages project preparation and prioritizing projects with employment and decent work, sustainability, industrialization, diversification and agriculture; financial and technical support; collaboration between home and host country agencies

- Encourages consideration of insurance, investment guarantees, including through MIGA, and new financial instruments. Encourages innovative mechanisms and partnerships

- Commits financial and technical support for project preparation and contract negotiation, investment-related dispute resolution, access to information on investment facilities and risk insurance and guarantees such as through the MIGA, as requested by LDCs

Latest developments

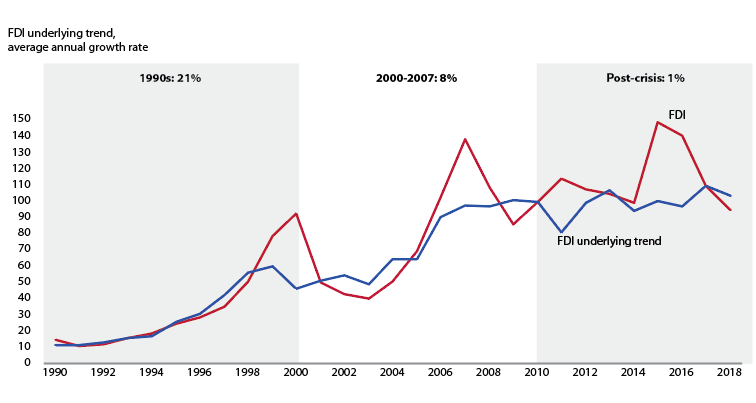

Foreign Direct Investment (FDI) has experienced anemic growth since 2008. Adjusted for short-term volatility and fluctuations caused by one-off factors, such as tax reforms, FDI has averaged only 1 per cent growth per year this decade, compared with 8 per cent in 2000-2007, and more than 20 per cent before 2000. In 2019, global FDI remain flat at an estimated $1.39 trillion. In 2020, the downward pressure on FDI caused by COVID-19 is expected to be -5 to -15 per cent (compared to previous forecasts projecting marginal growth in the underlying FDI trend for 2020-2021). The impact on FDI would be concentrated in those countries that are most severely hit by the epidemic, although negative demand shocks and the economic impact of supply chain disruptions could affect investment prospects globally. Lower profits from many multinational enterprises would also translate into lower reinvested earnings (a major component of FDI).

FDI inflows and the underlying trend, 1990–2018

(Indexed, 2010 = 100)

Source: UNCTAD, World Investment Report 2019.

Technological change has been a driver of the underlying trend of low FDI. Digitalization has enabled multinational enterprises to generate sales abroad with limited local presence. It has also facilitated a shift of international production from tangible cross-border production networks to intangible value chains and non-equity modes of operations, such as licensing and contract manufacturing. This is reflected in the much faster growth of trade in services and international payments for intangibles (royalties and licensing fees) than for tangible production indicators such as FDI and trade in goods. The growth of foreign sales of the top 100 multinational enterprises outpaces growth in foreign assets and employees, suggesting that these enterprises are reaching overseas markets with a lighter operational footprint, which might create challenges for local authorities to collect taxes.

Another long-term trend is the growing share of FDI flows towards developing economies. In the ten years prior to the 2008 crisis, developing economies attracted 30 per cent of global FDI flows, on average. This percentage increased to about 45 per cent in the last ten years, and exceeded 50 per cent in 2018 and 2019. Yet, these flows have not benefitted all countries equally. While certain regions have been able to attract more investment, particularly in Central Africa, South-East Asia and East Asia, in other regions, FDI declined below pre-crisis levels.

Read more on investment trends here.

Relevant SDG indicator

- 8.7.1 Proportion and number of children aged 5‑17 years engaged in child labour, by sex and age

- 8.8.1 Frequency rates of fatal and non-fatal occupational injuries, by sex and migrant status

- 10.b.1 Total resource flows for development, by recipient and donor countries and type of flow (e.g. official development assistance, foreign direct investment and other flows)

- 17.5.1 Number of countries that adopt and implement investment promotion regimes for least developed countries