The Addis Ababa Action Agenda includes commitments on reducing illicit financial flows (IFFs), as a necessary measure to raise domestic resources. It identifies tax evasion and corruption as particular areas that need both domestic and international action.

Specifically, in the Addis Agenda, Governments:

- Commit to redouble efforts to substantially reduce IFFs by 2030, with a view to eventually eliminating them, including by combating tax evasion and corruption through strengthened national regulation and increased international cooperation

- Invite other regions to carry out exercises similar to the High Level Panel on Illicit Financial Flows from Africa

- Invite appropriate international institutions and regional organizations to publish estimates of the volume and composition of illicit financial flows

- Commit to strive to eliminate safe havens that create incentives for transfer abroad of stolen assets and IFFs

Latest developments

In early 2019, the United Nations Conference on Trade and Development and the United Nations Office on Drugs and Crime (UNODC)—the joint custodians of SDG Indicator 16.4.1 on illicit financial flows—established a Task Force on the Statistical Measurement of Illicit Financial Flows, composed of representatives of official statistics, tax and customs authorities of several countries in Europe, Africa and Latin America, as well as international institutions, including Eurostat, the IMF, OECD and the United Nations Economic Commission for Africa.

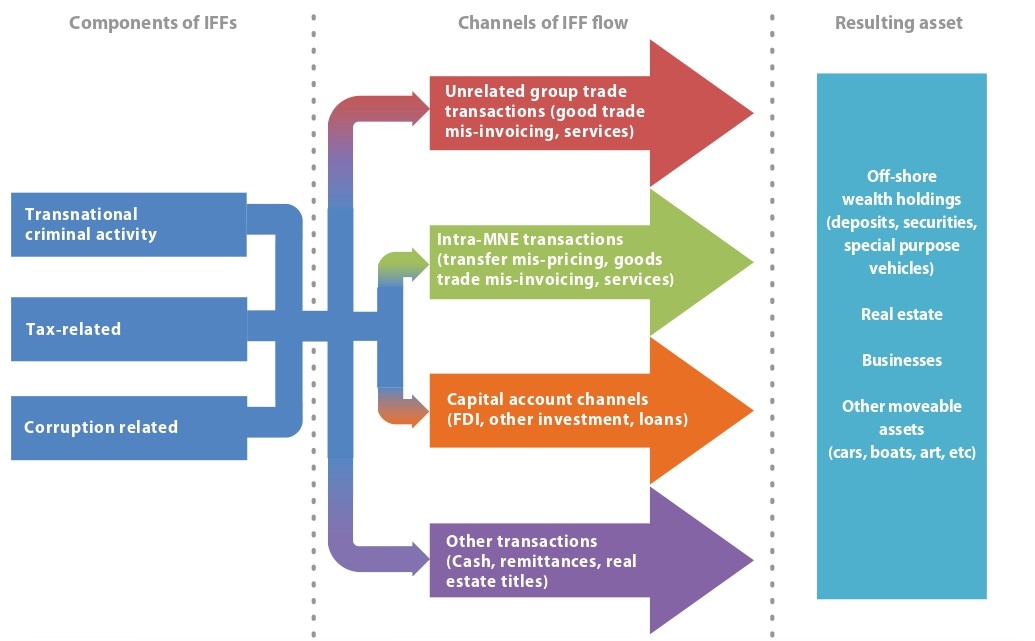

A conceptual framework for IFFs, including a concise definition and typology to define the scope of measurement was submitted to the Inter-agency and Expert Group on SDG indicators (IAEG-SDG), which develops the global indicator framework for the SDGs. In October 2019, the IAEG-SDGs endorsed a reclassification of the indicator to Tier II, signifying that it is conceptually clear, has an internationally established methodology and standards, but that data is not yet regularly produced by countries. This framework defines IFFs “as financial flows that are illicit in origin, transfer or use; that reflect an exchange of value instead of purely financial transactions; and that cross-country borders.” Four main categories of IFFs are identified in this conceptual framework, according to the activity generating them: tax and commercial practices, illegal markets, theft and terrorism financing, and corruption. In essence, it further refines this Task Force’s schematic approach (see below), by dividing IFFs related to criminal activity into two separate categories: (i) illegal markets and (ii) theft and terrorism financing.

Schematic diagram of illicit financial flows

Source: Inter-agency Task Force on Financing for Development.

Note: Resulting asset will be considered a ‘stolen asset’ if it is the product of corruption-related IFFs. Components of IFFs include both source of funds and motivations of IFFs and may not be mutually exclusive. Individual transactions from different channels may be combined by actors to try to obscure the source, motivation and/or use of funds. Arrows do not represent estimates of the magnitude of flows, and are illustrative rather than comprehensive.”

The next steps include the development of statistical methodologies to underpin estimations at country level. These estimates will shed light on the most appropriate statistical methodologies to estimate IFFs and provide additional evidence to help policymakers prepare or target interventions.

In early March 2020, the President of the General Assembly and the President of the Economic and Social Council jointly launched a High-level Panel on International Financial Accountability, Transparency and Integrity (FACTI Panel). The panel will produce an interim report outlining its analysis in July 2020, and its final report providing recommendations in February 2021. The General Assembly is organizing a Special Session on corruption in April 2021.

Read more on illicit financial flows here.

Relevant SDG indicator