The Addis Ababa Action Agenda commits States to make sure that all companies, including multinationals, pay taxes to the governments of countries where economic activity occurs and value is created.

In the Addis Agenda, Governments:

- Commit to reduce opportunities for tax avoidance, and consider inserting anti-abuse clauses in all tax treaties

- Note that countries can engage in voluntary discussions on tax incentives in regional and international forums to end harmful tax practices

Update from the 2019 Financing for Sustainable Development Report

A major challenge to revenue mobilization in both developed and developing economies is the ability of MNEs to avoid taxes through base erosion and profit shifting (BEPS), using highly sophisticated techniques to artificially move profits to different jurisdictions without any changes in the underlying real economic activity. Two new estimates published in 2018 present evidence that the sensitivity of profit declarations with respect to tax rates is greater in developing economies than in developed countries, indicating that BEPS is a relatively more important problem in developing countries.

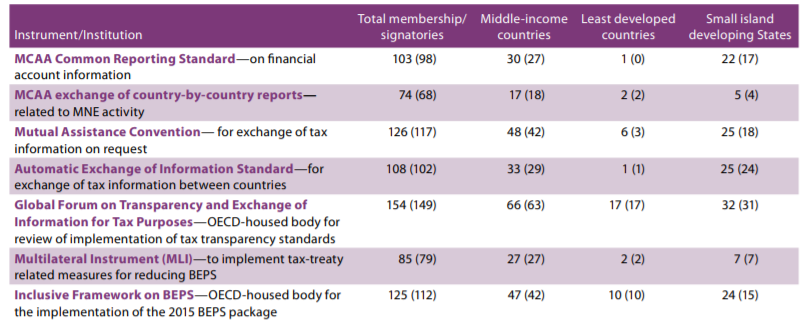

This challenge is compounded by developing countries’ higher reliance on corporate tax revenue. To reduce the scope for profit-shifting, the international community has undertaken a range of initiatives, such as the OECD-G20 BEPS project and the OECD-housed Inclusive Framework for BEPS implementation. Participation in these and other related initiatives is summarized below.

Participation in international tax cooperation instruments, 2019

(Number of countries)

Source: OECD.

Note: Figures as of 31 December 2018, previous year figures in parenthesis. Two countries graduated from middle-income status between 2017 and 2018, so were included in last years’ figures for middle-income countries but not in the end-2018 figures.

Read more on international corporate tax avoidance here.

Competition to attract private investment can lead to a race to the bottom in corporate income tax rates. Such tax competition can be particularly salient in developing countries, which often rely more on corporate taxation (figure 8). Replacing lost tax revenues with other forms of taxation may worsen inequality and, given the declining labour share of income (see chapter I), it may become increasingly challenging in some countries to raise tax-revenue-to-GDP ratios. This emphasizes that Governments wishing to attract investment through incentives–or to mobilize revenues through adoption of anti-tax-avoidance measures–can do so more effectively if they coordinate, at least regionally, to implement rules as a group of countries so that negative spillovers can be reduced. One of the proposals for tax reform in response to the digitalization of the economy could serve to reduce tax competition pressures by instituting a minimum tax scheme

Read more tax incentives and competition for investment here.