In the Addis Ababa Action Agenda, international cooperation to combat tax evasion and tax avoidance are important subjects, forming a significant part of the negotiations.

The Addis Agenda specifically:

- Commits to enhance disclosure practices and transparency in source and destination countries, including through transparency in all financial transactions between Governments and companies to relevant tax authorities

- Commits Member States to make sure that all companies, including multinationals, pay taxes to the Governments of countries where economic activity occurs and value is created

- Encourages countries to work together to strengthen transparency and adopt policies, including: MNE reporting country-by-country to tax authorities where they operate; access to beneficial ownership information for competent authorities; and progressively advancing towards automatic exchange of tax information among tax authorities as appropriate, with assistance to developing countries, especially LDCs, as needed

- Stresses that efforts in international tax cooperation should be universal and should fully take into account the different needs and capacities of all countries

- Welcomes on-going efforts, including the work of the Global Forum on Transparency and Exchange of Information for Tax Purposes; takes into account OECD work on BEPS

- Decides to further enhance the resources of the Committee of Experts on International Cooperation in Tax Matters to strengthen its effectiveness and operational capacity; increase the frequency of its meetings and its engagement with the Economic and Social Council through the Special Meeting on International Cooperation on Tax Matters; urges Member States to support the Committee and its subsidiary bodies through the voluntary trust fund

Latest developments

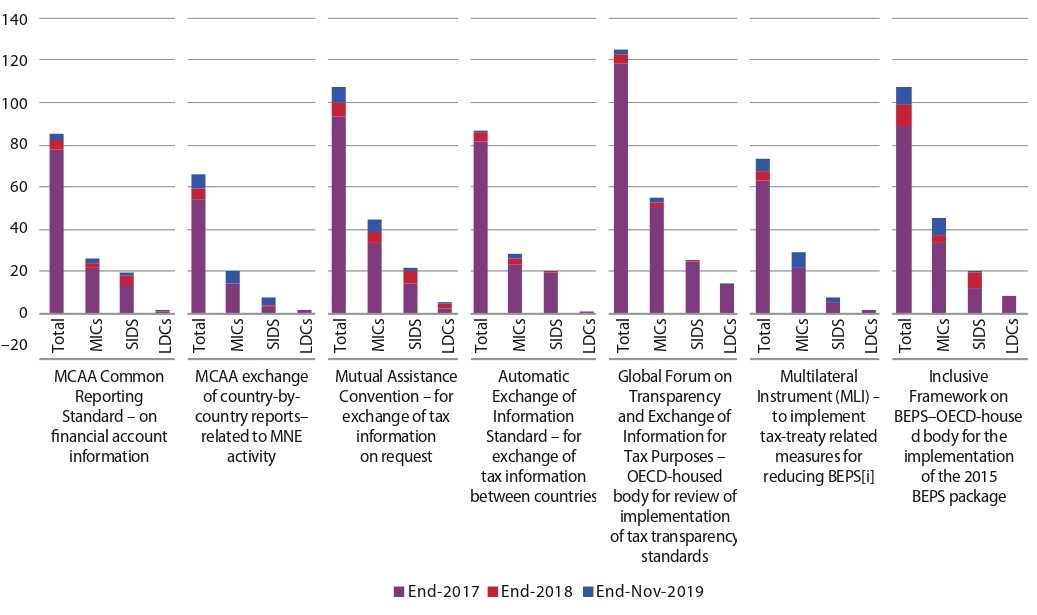

Many developing countries do not participate in international tax cooperation instruments, with slow growth in participation since 2017. LDCs in particular lag significantly behind in their participation. For non-participating countries, most of which have not had a role in shaping the underlying tax norms, choosing whether to participate requires an assessment on multiple dimensions, which may include whether the rules are well adapted to their circumstances, whether they have the capacity to implement the rules effectively, and the possible opportunity costs of deprioritizing other potential tax policy or administrative reforms.

Participation in international tax cooperation instruments, 2017–2019

(Number of countries, cumulative)

Source: OECD.

Note: Middle-income countries (MICs). Small island developing States (SIDS). Least developed countries (LDCs). Multilateral Competent Authority Agreement (MCAA).

The Global Forum on Transparency and Exchange of Information for Tax Purposes conducts peer reviews of all its member jurisdictions for compliance with international standards for transparency and exchange of information for tax purposes. A survey of Global Forum members provides indicative information that exchange of information requests have been increasing over time. 95 members of the Global Forum have begun exchanging financial account information automatically. Information on 47 million financial accounts with a total value of around €4.9 trillion were exchanged through 4,500 bilateral exchange relationships in 2018. The number of bilateral relationships grew to over 6,000 in 2019. In aggregate, middle-income countries now have over 1,500 relationships for receiving information, although no LDCs are receiving data from automatic exchanges. A number of developing countries have either elected not to receive information or have not yet passed the confidentiality requirements to be able to receive.

As of end-2019, over three quarters of the members of the Inclusive Framework on Base Erosion and Profit Shifting (BEPS) have introduced a country-by-country reporting filing requirement. As a result, substantially every MNE with consolidated group revenue above €750 million is now preparing country-by-country reports for their home jurisdiction. However, host jurisdictions can only get access to non-local country-by-country reports by agreeing to another international instrument and having a bilateral match. At end-November 2019, there were more than 2,000 bilateral exchange-of-information relationships for country-by-country reporting; 933 of these involve middle-income countries, up from 745 in 2018 and 477 in 2017. Currently no LDCs receive country-by-country reports through information exchange.

In other areas, discussions are ongoing in the United Nations Committee of Experts on International Cooperation in Tax Matters’ Subcommittee on Tax Challenges Related to the Digitalization of the Economy. The United Nations is holding a large workshop in September 2020 to build the capacity of developing country officials who will be advising their ministers and participating in the international negotiations on taxation of the digitalized economic activity. This capacity may also help authorities engage in regional tax cooperation mechanisms to coordinate measures, as well as consider alternatives in case no agreement is reached. Norms that are better adapted to developing-country capacities will necessitate less capacity-building, and thus may more quickly deliver financial returns in terms of increased revenue.

Read more on the progress on tax transparency and taxation of the digital economy here.